I have a hobby I enjoy called saving money. It doesn’t take much time and can even help fund my other hobbies.

The short version is – if I’m going to spend money anyway and 5 minutes of effort will reduce the cost, I might as well do it.

Here are a few recent examples.

Fun Money Hacks I Have Done Recently

Travel

Travel is fun. Paying less for the same travel is more funner.

Flights

We are going to Mexico for spring break this year. When Google flights finally notified me that the price had dropped below my target I made the purchase.

Savings for waiting: $41 * 4 = $164

But… the price on the airline website was $30/person higher than what I saw on Google. Why? Turns out the price for booking 4 seats in a single reservation was higher than making two reservations for 2 seats.

So we have 2 reservations.

Savings: $30 * 4 = $120

Checked Baggage Fees

We have one of those airline credit cards with an annual fee ($75.) I was going to cancel it before this year’s annual fee came due… but then I bought those 4 tickets to Mexico.

Since we travel with 2 kids we almost always check bags (typically two of them.) It’s just way more convenient. Well… said airline card waves all baggage fees, so I am keeping this card for another year.

Savings: $35 * 2 bags * 2 flights (roundtrip) – $75 annual fee = $140 – $75 = $65

Cash Back on Hotels

I booked our Mexico hotel back in October when Rakuten was offering 2% cash back on hotels.com (typically 1%, excluding taxes and fees.)

(Good thing too because now the hotel is sold out for the length of our stay.)

Total was $1,192.68, or $909.44 for the room plus a bunch of taxes. 2% back on that $909.44 will earn $18.19 once we complete our stay.

I made this payment via Paypal with my Chase Freedom card since Paypal was a 5% cash back category in Q3’23, which earned $59.63.

Savings: $18.19 + $59.63 = $77.82

If you haven’t used Rakuten before you can get $30 cash back after you spend $30 (on the stuff you were buying anyway.) (affiliate link)

Just Because of 5% Interest Rates

Once interest rates drop I’ll have to find another way to entertain myself, but in the mean time…

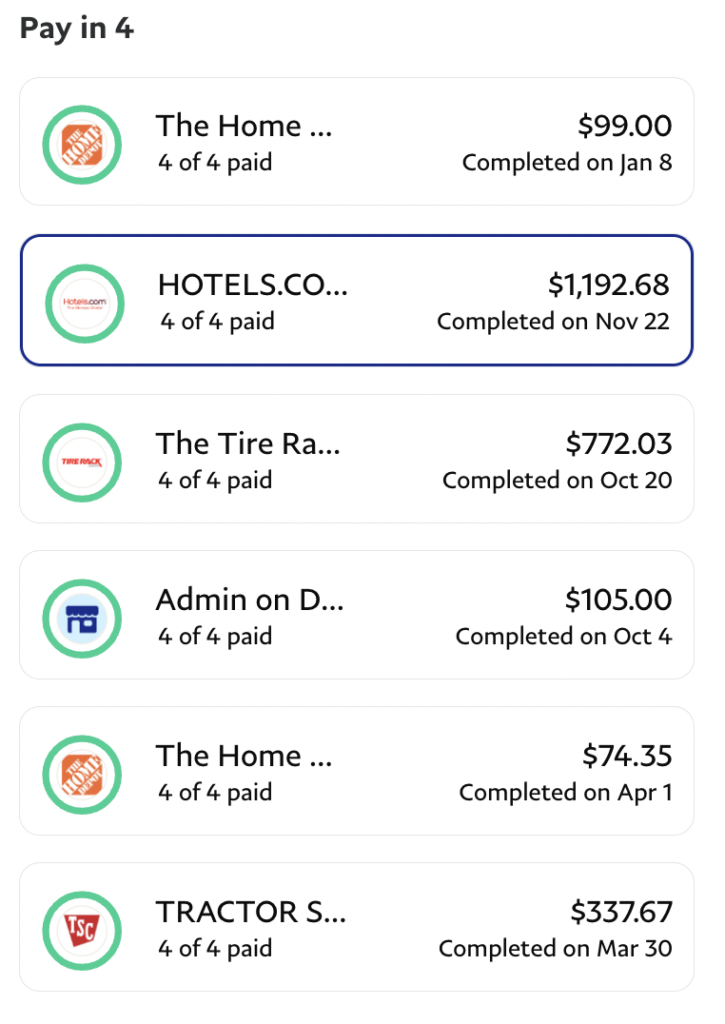

Pay in 4 via Paypal

Usually when I pay for something via Paypal I automatically select the Pay in 4 option. This splits the cost into 4 payments, 1/4 up front and then 1/4 biweekly (~6 weeks total.)

All this means is that a purchase is now spread across at least two (but sometimes 3) credit card billing cycles for a 60 to 90 day delay. It is nice for cash flow management.

If on average I get a free loan for an extra 60 days, then I can keep that money in my cash account a little longer earning 5%.

In this purchase history I spent $2,580.73 x 5% * 60/365 = $21.21

It’s not much… but it happened automagically with the click of a button so the hourly rate was good.

Savings: $21.21

Time Shifting via Pay in 4

A greater benefit was had just from time shifting 3 of the payments into Q3… so instead of 1% or 1.5% I was able to get 3% on 3/4 of this purchase.

Savings: 3*$193.01 * 5% = $28.95

My Chase Plan®

Chase credit cards offer a pay over time feature which they promote as “no interest” but with a monthly fee. How that is different than charging interest is beyond me, but what can you do.

But sometimes… that fee is zero. I don’t know why or when, but multiple times now I’ve been able to snag some good interest free loans. Most recently I paid some property taxes on my Freedom card solely because I was being offered these no fee pay plans. Now I have 2 years + 2 months of 0% interest

I’m skeptical that I will be able to earn 5% for the next 24 months due to Fed rate cuts…. but if I can, I’ll get $310.

Playing the Spread

With his/her new Discover credit cards we were able to borrow ~$19,500 for 18 months+/0 at 0% interest. I invested this in short-term treasuries yielding 5%+

See: Playing the Interest Rate Spread for an Easy $2,000

Earnings on investment: $19,500 * 5% * 1.5 years = $1,462.50 (plus another $500 in cash back on purchases)

3% Balance Transfers

That airline card I mentioned at the beginning of this post… they just recently offered balance transfers with 0% interest until February 2025 (13 months) with a 3% balance transfer fee.

It’s not 0%… but what the heck, I’ll take the 2%-ish delta and put that in my pocket. I had done this previously ~18 months ago with ~$25k when the SP500 was 25% lower so as to avoid selling stock during a significant downturn.. and now those balances are coming due with about $10k remaining.

Total fee: $300

Interest earned on $10k for 13 months: 10k * 5% * 13/12 = $542

Total earned: $242

Gift Cards

These were easy and rewarding

Airbnb Gift Card at Costco

We are going to Europe this summer for a few weeks and are staying in some Airbnbs. Over Christmas, Costco was selling $500 Airbnb gift cards for $450.

The only downside was it was only one per customer.

Savings: $50

Target Gift Card

Every December as far back as I can remember, Target has an offer for a single $500 gift card for $450.

Since we routinely spend more than $500/year at Target I usually pick one of these up.

But this year… Target purchases were one of the 5% cash back categories on Discover cards, so of course I made the purchase on that card. And since Discover is offering 2x cash back on all purchases for the first year… the savings are a little higher.

Savings: $500 – $450 + 10% cash back = $50 + $45 = $95

Starbucks Gift Card

Around Black Friday Starbucks had a promotion where you got a $5 gift card if you purchased a $25 gift card. We don’t really do Starbucks much because coffee at home is so much better, but I do like a peppermint mocha around the holidays. We also occasionally stop for a hot chocolate after a snowboarding trip.

Then I accidentally found out about a promotion where you could get a $3 grande beverage every Thursday afternoon in January… and by coincidence Jr had some sports stuff on Thursday afternoons just near a Starbucks, so I used this weekly.

Savings: $5

Lowe’s Gift Cards via Target Circle

Every once in awhile Target has a promotion… complete 3 separate transactions of $100 or more and get $30 credit for future Target purchases.

I use this to buy Lowe’s gift cards whenever I have a project underway (almost always?)… by paying with our Target credit card we get 5% off, so I can buy a $100 gift card for $95.

Do that 3 times and I get an extra $30.

Total savings: 3 x $5 + $30 = $45 (Ultimately 15% off on everything at Lowe’s – or anywhere really.)

Not included in my math here, but sometimes these can be stacked with other offers for extra savings

For more discount gift cards and a free $5 with purchase, check out Raise.com

Bonuses

Getting paid to click a few buttons on the phone.

Amex Send & Split

Amex Send & Split had a promotion where if you sent $30 to a Venmo user they gave you $10. You could send it to anybody so I just sent it to my wife… keep it in the family, ya know?

It only took 3 minute to setup and I now use it all the time for paying the nice people who clean our house via Venmo.

Earnings: $10

Pay Utilities with a Credit Card

A few different times now we’ve had an offer to get $10 for paying a $100 utility bill on Chase cards. It takes me 2 minutes to click the enroll button and then point the autobiller to a different credit card.

Earnings: $10 * 3 = $30

Notably Absent – Bank bonuses

In the past when interest rates were 0% I would occasionally jump through some hoops to get a bank bonus… the process is typically:

- open a new bank account

- deposit some money for a period of time

- get paid hundreds of dollars

But when interest rates are 5% and these new bank accounts typically pay nothing aside from the bonus, it just isn’t worth it to move money around imho.

See: Bonus Season!

For the Long Term

A good(?) move when interest rates were low and inflation was high.

Investing the Mortgage

I borrowed money against the house at 2.75% and invested it, primarily in the US stock market. As of the end of 2023 we are up $3,170 after accounting for all income and expenses.

Probably this year the dividend income will start to completely cover the interest expense and over the next 28 years inflation will do its thing in our favor.

See: Investing our Mortgage – 2 year update

Summary

I have a fun hobby that makes a little money and that I can do in the car while waiting for kids to finish school or sports. Silly? Certainly. Irresponsible? Probably.

But just in the examples above I’ve got $1,257.98 in savings or interest, another $1,462.50 from our Discover credit card loans (plus the cash back, not included), and $3,170 in investment returns from investing the mortgage.

Add that all up and we are talking some real money. Clickity click $ $

I am always getting deals on my gift cards through both Kroger’s (for the gas points when cards are 4x the points) and sites like AARP ($500 Carnival gift cards for $450 as an example). Depending on who is giving me the highest cash back, either 5 or 6% in any given month, use that credit card for purchasing.

Wanted to add another cruise to go with one we already have scheduled in Jan 2025 (other cruises are scheduled as well in 2024 but adding on in January was tempting, with the holidays over and the kids back to school). The Carnival website wasn’t offering much but the consolidator website I use in addition to Carnival was offering $100 onboard credit (OBC) for the price of the fare, as well as an additional $200 OBC for it being a seven day cruise. Tag on my $100 OBC for being a Carnival shareholder and that’s an additional $400 OBC on top of a rate that was equal to or less than Carnival. Pays for some extras onboard.

And you didn’t even mention turning that Discover cash back into more by using it for gift cards. For example, $50 in Discover cash back yields a 10% bonus (so, $55) at Lowe’s…

Good point! Those bonuses are nice

Hey,

Have you tried selling tradelines?

Regards

I have not and don’t really plan to. I’ve seen some examples of people making a lot of $ with these but there is the risk that your accounts get shut down

I tend to not bother with the low dollar stuff, but I’m still working, so I focus on credit card and bank bonuses. I agree that bank savings account bonuses aren’t worth it (except for Chase’s $900 bonus), but if you have a direct deposit you can change easily, you can get great returns just for opening, changing you DD, transferring, and closing checking accounts for bonuses. I did 15 accounts last year, my first year doing it, and netted $4,500 taxable. Doctor of Credit is a great resource.

“Doctor of Credit”:

https://www.doctorofcredit.com/targeted-chase-900-checking-savings-bonus/

https://www.chase.com/personal/savings/savings-account/interest-rates

All Balances 0.01%

= (900 / 15000) * (366 / 90)

= 2.44% simple interest annually.

Seems to be savings accounts in USA which pay larger interest rate more straight forwardly:

https://www.bankrate.com/banking/savings/best-high-yield-interests-savings-accounts/

Exactly, this is what I meant by bank bonuses often not being worth it when there are high yield alternatives.

5% >> 2.44%

I think the 2.44% rate is incorrect.

The comparison would be $900 earned in interest on $15,000 principal in 3 months. This would be an annualized earnings of $3,600 (if you could do the bonus 4 times in a row, which–of course–you can’t).

$3,600/$15,000 is an annual interest rate of 24%.

A money market fund earning 5% would only earn you $750 on $15,000 over a year.

Is my math wrong?

Of course, you would want to move the money out of Chase after 3 months (with the $900 bonus) and move the money to a MM fund or other investment.

I agree that bank bonuses are often more trouble than they are worth.

Thanks for your blog!

My arithmetic is crook.

24.4% annualised simple interest it is.

Posting in haste is not helpful.

Ha, you are correct. Decimal place is off.

Presumably why AnotherEngineer said this was the bank bonus worth doing.

Moral of the story: always double check the math :)

I generally agree with the low $ stuff but I figured the hourly rate is still quite good.

What do you figure you would have earned just leaving the direct deposit money in a high yield savings account (5%+/-)?

It isn’t quite that good as $300 is for an easy single DD checking account bonus and $600 is if you do that and the savings, so 16% if you pull it out on the exact day. So $15k yields $600 in Chase vs $187.5 in a 5% HYSA for three months. As noted, there probably isn’t something similar to roll that money into. There certainly are current savings bonus offers that are less than a HYSA with more work that may have made sense a year or two ago though.

Thanks for sharing your hacks!

I’ve got two hacks right now:

(1) Shop Your Way credit card from Citi. The normal cash back isn’t that exciting HOWEVER they send great promos. I’m getting 10% statement credit on groceries, gas and restaurants for the rest of the year – as long as I spend between $1,000 – $2,00 a month. I’ve also gotten targeted for offers for online shopping and utilities.

(2) I have a large target order coming up so I’m buying target gift cards with my shop your way credit card at the gc to cover the purchase. You earn 1% back through target circle when using target gift cards instead of your target card. So instead of getting 5% back with target card, I’m earning 11% (10% w/ SYW and 1% with target circle).

That is a very nice targeted offer

The using cards strategy at 0% and investing in 5% yields is a cool idea, similar to the mortgage idea. The other ideas I’m not so sold on saving $15 or $20 here or there, but to you point if you’re just waiting for someone and that’s your version of social media scrolling, why not.

Costco does a solid on coupons, especially when buying non grocery items. We saved $100 on a kitchen faucet, $30 on a restaurant gift card, and $300 on a mattress. They don’t price match the website, but they have an awesome price adjustment request that they are pretty good about.

We also use the price scan tool on our credit card on if we buy something and it goes for sale later. Then we use that for fun money, like a coffee shop date.

I forgot to include in this post but Costco does offer those good deals on local restaurants… $75 for a $100 gift card or thereabouts. My wife has one of those in her wallet at all times just in case.

The small stuff I just think of as finding a $20 bill on the ground. I’m not too proud to take 10 seconds to bend over and pick it up. Thinking of it as an alternative to scrolling social media is good too!

I discovered a new hack today. We made a Priceline car rental reservation yesterday. Today the posted a $35 off coupon for a car rental over $250 (which the OG reservation was). I got on the chat and told them this the customer service person credit back $35 to my credit card.

My other not original hack is to use the area code of your present location and 867-5309 as the number for the grocery rewards card of the chain you are at. It is nearly always an account and you get the discount without filling out the form. Call Jenny

Can confirm. The phone number works. I was told this trick by a gas station attendant in Oregon while he pumped my gas! It’s a group effort to use the number to accrue points and get your grocery discounts and then also to cash the points in for a discount at the pump. :) For us Gen X who know the song hehehe.

You can further hack Amex Send by paying P2 (or yourself, at a different PayPal/Venmo account) the maximum $2000 every month, and having them do the same. There are no fees and no interest. I do it right after the statement closes so you’ve got about 7 weeks until you have to pay it back.

Smart! I just did this, thanks for the idea

2 of my AMEX cards are on 0% (one as an intro offer, one a pay over time promo). We’ve been sending that 2k per month as a more direct means of accessing the money, good to hear there are others out there :)

Can you explain this hack please? Is one supposed to putthe $2000 in a HYSA?

Yes

My car was totaled maybe a year and a half ago, so I had to get a new car. Got a 2.25% car loan. First, I had it in I bonds earning 7%-9%, sold the i bonds at the beginning of this year, opened a CapitalOne Savings account for a sign up bonus that will be 10% annualized for the 3 months the funds are there, after that I’ll throw it into a 5% cash account until I feel like paying off the loan. Wouldn’t mind having the cash flow back.

Most of the bank bonuses don’t require a meaningful amount of cash, usually a token balance and a direct deposit. I still find them worthwhile.

Just did Robinhood’s 3% IRA transfer match, got a bonus there that dwarfs anything else I’ve ever done – gotta hold my Roth IRA there for 5 years, but not an issue for me. I’m betting they’ll be acquired before then anyway.

The Robinhood transfer match sounds interesting. If I move $1 million dollars over they will give me $30k?

Those low rate auto loans are nice – we got ours at 2.74% which seemed like a steal at the time so I put 0 down (even financing registration, taxes, fees, etc…)

I also put zero down. I asked if there was a minimum down payment to get the rate, they said no, so I didn’t see a reason to provide a down payment.

Yes, you’ll get $30k on a $1M transfer.

Steps:

1.) Open Robinhood brokerage account (if you click through Rakuten you can allegedly receive $50 for depositing $100 in the brokerage, but it’s not an instant credit. Rakuten support told me T&C says 3 months.

2.) Sign up for Robinhood Gold, maintain Robinhood gold for 12 months. This costs like $7 per month.

3.) Transfer your IRA from whichever brokerage to Robinhood. Robinhood credits 3% of the transfer immediately upon receipt of the funds. You can buy an ETF with those funds the same day. It only took a couple days for my Roth from Schwab to get to Robinhood, transferred ETF by ACATS.

5 year hold requirement at Robinhood on your transferred funds + match, so maybe don’t send any funds to them that you’ll want to convert or withdraw within the next five years.

https://robinhood.com/us/en/about/retirement/

Thanks, this is enticing.

Conveniently one of the statements in the FAQ matches my question:

“For example, if you transfer or roll over $1,000,000, we’ll give you $30,000 on top.”

Do you think you are going to take advantage of the Robinhood offer? It’s enticing, but the 5 year lock up has me a bit concerned. I have a 401k I could roll over to an IRA that would net me a little over 30k.

I am seriously thinking about it. I left my 401k at my old employer because they have amazing fund choices (0.01% er on SP500 fund) but a 3% up front bonus would make it worth a change.

What concerns you about the 5 year holding period?

Yeah I still have a 401k through my old employer so I would want to do a rollover. Fidelity Manages it so I thought about doing a Rollover to an IRA first inside of fidelity and then doing an in kind transfer to Robinhood of the IRA. Seems like it would be out of the market less since a physical check wouldn’t need to be mailed to create the IRA at Robinhood, even though the total time may take a bit longer.

The 5 year holding period could let them change their fee structure etc, but it’s probably not too much of an issue. SIPC insurance is only 500k so that is a bit of a risk to if transferring a higher amount than that.

Rolling it over to an IRA would kind of kill future opportunity for backdoor Roth conversions though due to the prorata rule. However, I’m not sure that will be an issue for us in the future as I don’t know if we will get above the earned income level to enable backdoor Roths.

It’s not every day someone basically offers you a car to move your investment accounts over. And with compounding over 30 years this is over $220k of money

It is more concerns of Robinhood going belly up and then potentially risking such a large chunk of our retirement.

SIPC as insurance in general is probably overrated even at 500k. It is a small non-government entity with minimal reserves so couldn’t bail out even the smallest organization.

That said… Robinhood doesn’t own your investments. They aren’t accessible for their spending or to cover their debt. In the event of their bankruptcy you should be able to move your assets elsewhere. In theory.

I assume this promotion is their way of growing total assets in their system prior to attempting a sale to one of the big banks – it wouldn’t surprise me if they are owned by Chase or similar within 5 years.

So based on that do you think you would put a large amount way past the SPIC limits into the account? I keep going back and forth since it’s pretty easy money.

Curious if you ended up jumping on this promotion?

I didn’t. I didn’t really have the time or inclination to investigate properly. That, combined with a general distrust of Robinhood and a 5 year commitment… I just did nothing.

This is interesting. Do you think this is worth doing even if you don’t have an IRA to roll into Robinhood? Is the 3% match worth it as a stand alone bonus?

It’s hard to beat a free 3%, but the lower value the IRA the more the Gold membership fee eats into the total return (assuming only doing Gold to get the 3% match.)

Please write more about living abroad and paying taxes in two countries. I love to hear your tips about this since I’m planning on living fire abroad.

What have you read so far and what questions do you have?

Does the paypal pay in 4 allow you to use CC to make all 4 payments and still earn points?

Most of the no interest payment plans I’ve seen people use require you to use your bank account and the annualized interest rate can easily be >10% when factoring in lost 2%+ CC rewards.

Yes

I want to use My Chase Plan. Both P1 and P2 have a promo on the first plan of 0% fees. Does anybody know if that is for a specific card? How can you tell which, the offer appears on my credit score “offers” section

Also, I had a transaction at CVS during 5% PayPal- 3x $500 visa gift cards, paid via PayPal or code in cvs. It triggered 7x UR earnings due to the category bonus combined with the drug store bonus. That said, the $1517 transaction doesn’t give the option to pay over time…makes me nervous I’ll make a charge and then won’t actually be able to utilize the fee free plan. Any insights – transaction coded as paypal/cvs so maybe they are just restricted bc too cash like? How about Plastiq?

Promo offers usually for a specific card, yes. It should state which, although I figure it out just by clicking on previous transactions to see if the 0 fee option is available.

Paypal transactions work – I did it.

Wow – loved this post and I got some new ideas! Thank you so much for writing it. I went on a 2 wk challenge to see how many little ways like this I could find to earn money. I made $535! I was like, dang! Now I use so many of these (like Rakuten) in daily life. My spouse and I have now earned about ~$300 so far just with that. It is fun!

Not really worth the time but fun indeed

Excuse my ignorance as I’m trying really hard to learn how to optimize like everyone here, though could you explain how the split of the payments in 4 periods helps with that 5% versus just the lump sum?

With one of our credit cards the closing date is the 8th of the month. That balance is then due on the 5th of the following month.

If I made a $1,000 purchase on March 9th (the first day of the new billing cycle) I would have to pay it back on May 5th.

This already gives me about a month of float which is better than paying cash.

If instead this transaction was split into 4 equal payments, $250 on Mar 9, $250 on Mar 23, $250 on Apr 6, and $250 on Apr 20, then $750 is due on May 5th and $250 on June 5th.

I get an extra month of float for that $250.

It’s not a lot ($250 * 5%/12 = $1) but all I had to do is click a button so why not

I noticed you made a purchase at Tire Rack, which I also happily patronize. But you just bought your car not long ago – are these snow tires for your ski trips or replacement tires? I always like keeping the snow tires on their own rims, that makes swapping easier and avoids damage from un- and remounting the tires on the wheels.

replacement tires – the OEM tires are known to have a life of only 25k +/-

Do you have the snow tires on steelies? I’ve been thinking of getting a set but haven’t put much thought into it… we weren’t able to hit the slopes much this season.