Only 40 More Years of Working For That Bling Bling (photo credit – Achim Voss)

For somebody who has committed to building wealth through living well below their means and investing, how long will it take to become financially independent?

Often times we use simple rule of thumb calculations to make an estimate, projecting an average investment return until a 4% withdrawal rate will support a desired cost of living.

This has limitations, of course:

- The stock market is a volatile and uncooperative beast, so our assumption of constant growth never materializes. How do real world investment returns impact our wealth accumulation?

- Although I would recommend it, few people are willing to put 100% of their retirement savings in the stock market. Will a more “conservative” asset allocation be a boon or a boost?

- Despite the data, not everybody is comfortable with a 4% withdrawal rate. Some require a 3% withdrawal rate, or even (gasp!) 2%. How much longer will it take to save 33x or 50x our annual spending?

To answer these questions, I used the same methodology as the Trinity Study… but this time, looking backwards.

“How long would it have taken to become financially independent throughout modern history?”

Financial Independence: How Long Will it Take?

There are 3 primary factors determining how long is required to become financially independent through saving and investing, all of them inter-related:

- Savings Rate – What percentage of after-tax income is spent and thus gone forever?

- Asset Allocation – How are assets proportioned between stocks and bonds?

- Arguably a key factor in Investment Return ->

- Real Investment Return – A higher rate of return obviously increases wealth more quickly

Below I evaluate savings rates of 25% – 75% of after-tax income, asset allocation from 0% – 50% bonds (the remainder invested in equities), and investment performance since 1926.

A Good Savings Rate of 25%

The average savings rate in the United States is somewhere around 5%. Nobody will be retiring early with a 5% savings rate. So I begin this study with an example of someone already saving at a healthy clip of 25%.

I’ll go slowly through this first chart by focusing on some simple data points. This same chart format is used throughout.

First the bar-chart. If we had begun saving 25% of after-tax income in 1926, and invested it equally between stocks and bonds, it would have taken until 1959 (33 years) to become Financially Independent with a 4% withdrawal rate. The blue bar chart shows this uniquely for all years in our data set.

The red bar chart indicates how many additional years of saving 25% of income would have been required to increase assets to 33x total assets (a 3% withdrawal rate.) This would take an additional 3 years if we started saving in 1926; 36 years total bringing us to 1962.

The green bar chart shows the same for a 2% withdrawal rate. Again for 1926, it would take an additional 11 years to reach this lofty goal in 1973 (47 years in total.)

The purple chart (“75% stock”) shows the reduction in time to reach a 25x / 4% level if we increased our asset allocation from 50% to 75% stock. The “100% stock” line shows the same when we increase our asset allocation even further. (Note that in no year does a lower allocation of equities help us reach our FI goal sooner.)

The purple chart (“75% stock”) shows the reduction in time to reach a 25x / 4% level if we increased our asset allocation from 50% to 75% stock. The “100% stock” line shows the same when we increase our asset allocation even further. (Note that in no year does a lower allocation of equities help us reach our FI goal sooner.)

On average, saving 25% it would take a little more than 32 years to become FI with a 4% withdrawal rate and a 50% stock / 50% bond asset allocation.

Increasing assets to 33x would add an additional 5 years on average, but as many as 19. To 2% would take 8 more years on average, but as many as 22.

Increasing the proportion of stocks to 75% reduces time to FI by 4 years on average, and to 100% reduces it by an additional 3 years. However in many years the reduction is substantially greater.

Increasing Savings Rate to 50%

Increasing savings rate implies two things:

- More of each paycheck is invested rather than spent

- Cost of living is lower, so fewer assets are required to become FI

Win, win. This is obvious from the chart. Pay special attention to the y-axis; FI has accelerated by as much as 20 years

Average time to reach a 25x asset level is only 17 years. An additional 3 and 5 years are required to reach 33x and 50x, respectively, on average.

Average time to reach a 25x asset level is only 17 years. An additional 3 and 5 years are required to reach 33x and 50x, respectively, on average.

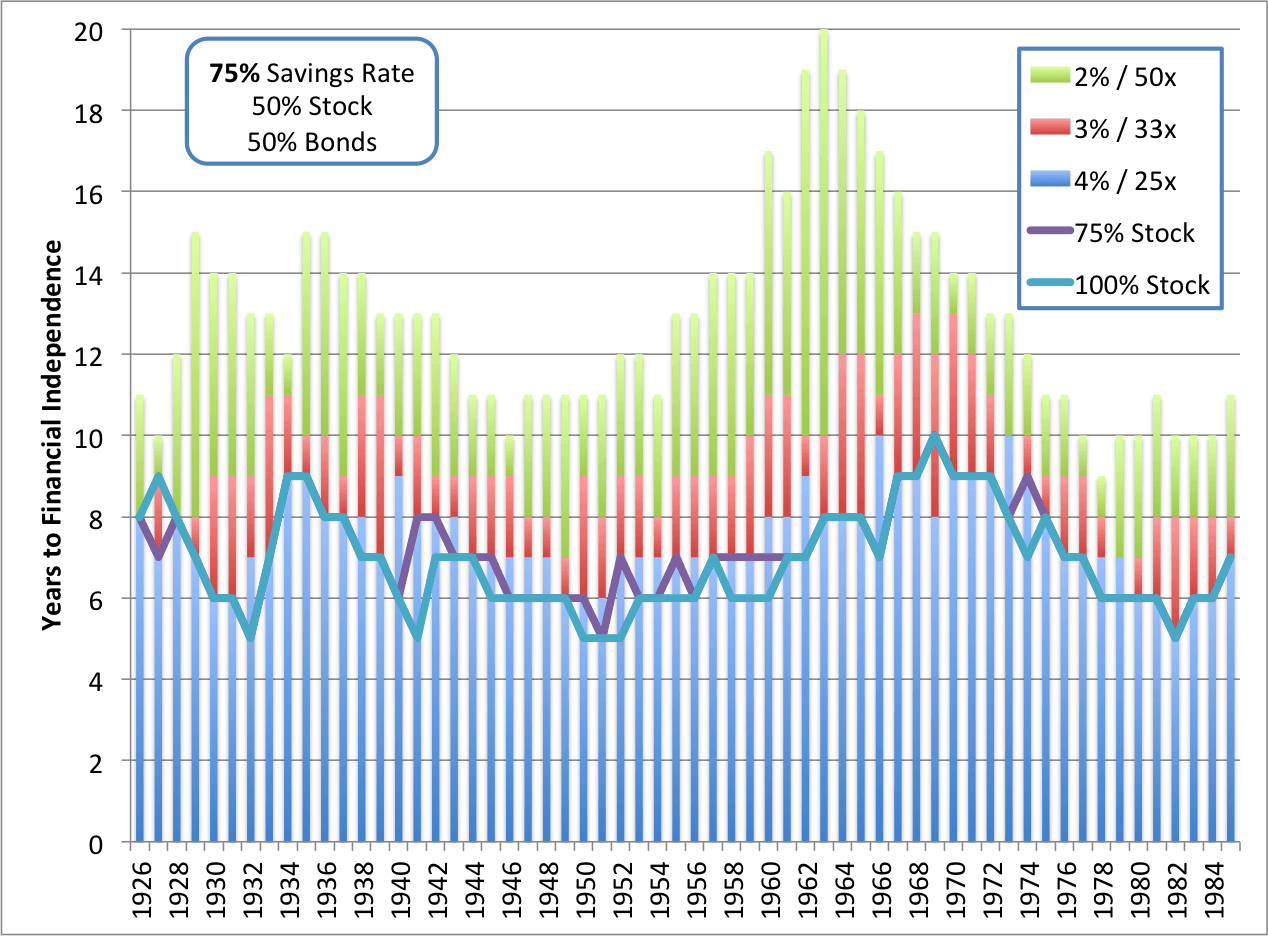

A 75% Savings Rate

When we were doing our accumulation heavy lifting, we were saving 70%+ of after-tax income. For a few years I even deposited my whole paycheck into our brokerage account.

At this level of savings wealth grows rapidly, and things like interest rates, stock market return, and even asset allocation are almost irrelevant.

With a 75% savings rate, the time required to accumulate 25x annual spending averages only 7.5 years. An additional 2 years will get you to 3% / 33x, and 3.5 years on top of that will get you to 2% / 50x.

With a 75% savings rate, the time required to accumulate 25x annual spending averages only 7.5 years. An additional 2 years will get you to 3% / 33x, and 3.5 years on top of that will get you to 2% / 50x.

We were aggressively saving for 10 years, so despite the occasional disbelief that it is possible we were actually below average.

Ancillary Data

Working assumptions:

- All examples assume an initial net worth of $0. Those with non-mortgage debt first need to get to zero. Those with assets will have a shorter path.

- Annual Income is constant when adjusted for inflation (the corollary of a constant withdrawal rate post retirement.) Increasing income faster than inflation can provide a boost as long as lifestyle is not also inflated.

- Taxes are a constant percentage of total income. Investments are inside a tax sheltered account. Reducing today’s tax burden can provide an additional boost as long as the tax savings is invested.

- Investment fees considered part of annual spending. Our fees are less than 0.08%, or about $800/yr/$1 million. (Check yours with Personal Capital.)

The statistics for all 3 charts are shared here for those interested.

Statistics

Conclusions

By far the most important variable in becoming Financially Independent is Savings Rate, even more important than return on investment. There are massive financial advantages to living simply and efficiently (amongst the numerous non-financial benefits.)

This is great news for young people who want to retire early, but also for late starters who want to secure their financial future before reaching traditional retirement age. It is never too late to start or to reverse lifestyle inflation.

The higher the savings rate the greater the benefits. For example, while saving 75% it is possible to accumulate even 50x in less time than it takes to accumulate 25x while saving 50%. Highly conservative individuals would obtain a greater security benefit through increasing savings rate versus working longer.

Asset allocation also plays an important role. The higher percentage of total assets allocated to equities, the faster wealth accumulates. So much for risk-adjusted returns. This impact is most significant for people saving a small percentage of income, but is also notable for those striving for assets of 33-50x spending.

tldr; Savings rates of greater than 25% are required to achieve financial independence through savings and investing. A greater allocation of assets to equities and higher savings rates accelerate FI.

Damn, i love your posts! :D

Even though I can never reach a 75% savings rate, I may be able to reach 50% in the next 10 years! Your posts always keep me motivated.

All the best from germany,

Finn

Tausend dank!

50% would be great. Increase income as much as possible while reducing (and eliminating) expenses

It helped when by the time Winnie and him get to save 75%, he probably was making closer to 6 figures and the last few years was $130k plus all the perks and bonuses that come with the job. :)

That’s why my friend who had 7 years head start, she worked immediately right after high school and still quite broke as her salary doesn’t get the big jump like a college grad would.

Combination of saving, if you don’t have the gut to start your own business, then you need to get a practical degree to have the salary boost. It’s easier to live off 4% of $1M, than 4% of $200k.

In my mid 40s and retired. Could have at 40. :)

Very nice. Congrats!

How did you do that?

Trying to increase my percentage every year and buying stocks on sale lately. If we get another uptick by 10-20% again in the near future, I will be nearing the 25x mark very soon!

Just another data point to empirically confirm your analysis. We saved 50% to 75% for around 10 years and hit FI at that point. Guess we’re pretty average… :)

No one ever believes it’s possible to reach financial independence in 10 years or so, but with huge wages in some areas of the country and in some occupations, it’s not that hard. If you’re making $200k or $300k as a household, just live like someone “only” making $50-75k and you can hit the savings rate needed to hit FI in not much more than 10 years.

very true indeed. We did this for two years preceding FI and left FT work at 36 and 34. Now my wife does PT consulting from home and I work PT at a non-profit focused on providing affordable housing. In my “spare” time, I’m building our house (while we live with family for free). Our portfolio was somewhat meager (~$500K) compared to others like you at the same point. But instead of receiving years of matching 401k contributions, I received an inflation adjusted military pension which has taken the worry out of SWR etc. Couldn’t have done it without getting expenses under control though.

Fortunately the test is only Pass / Fail so average is good enough :)

Now *this* is a post to refer people to over the coming decades!

Maybe you can wave this in the Mad Fientist’s direction (or Cooley et al’s :-) and provoke him into filling some of the intermediate savings rate percentages between 50% and 75%. At what rate *does* asset allocation become effectively irrelevant?

PS I’ve linked to this post over at Reddit /r/financialindependence — apologies in advance to your server farm and network bandwidth bills ….

Bring it on! Haha

Thanks Joseph.

Awesome work, Jeremy, as always! Biggest takeaway for me here is when you said that savings rate > return on investment… I think that’s a strong argument against active equity investing (trying to beat the market). Do you agree? When the market is always going up, up, up as it has for the last several years, it’s easy to put your feet up and argue for passive equity investing, but it will be harder for me personally to resist getting more active (trying to pick individual winning stocks) when the market stagnates/declines. So part of what I’m taking away here is, even when the market is down, resist the urge to pick individual winners and instead focus on optimizing your savings rate.

People always think of Buffett as a great investor because he averages 15% return every year (I’m just making up a number)… but maybe a 15% reduction in my household costs is even more beneficial to reaching financial independence than a 15% investment return… that it’s better to save like Jeremy than to invest like Buffet. I don’t have the number skills to prove this or illustrate it, but maybe you do? :)

I think the strongest argument against active investing is that over a long time period nobody beats the market. Everyone tries at least once though.

Buffet is also well known as a

tightwadfrugal guy, so maybe the answer is both. This is in essence what a higher allocation of equities does (increase the CAGR.)I’m 28 (married, she’s 27) and we should be FI in 7 or 8 years. Currently saving around 55% of our income and that will continue to increase as salary increases. Once we pay off our cars in another 33 months (0% and 1.9% interest), we’ll invest the payments. They were a mistake to buy, but I learned my lesson and will keep them until they die or until we sell them to travel the world!

Are there any calculators or way to estimate time to financial independence if you already have a jump start on your savings? Although we just started our FI journey we are well above the zero starting point so I would love to see a calculator that takes this into account.

You could somewhat hack the use of cFIREsim.

Set Portfolio Value = Current Savings and Yearly Spending = 0. Then add an inflation adjusted pension that starts in the year of retirement (e.g. 2015) equivalent to your annual savings. This will add $X per year to your portfolio per the target asset allocation.

On the output page, you would have to manually look for your Retirement Number, but it would at least give you a rough idea.

Edit: All of the recommended calculators shared so far all use a fixed rate of return. Historical sequence of return data is what I used for this post’s analysis, and ideally is what would be used to estimate time to retirement (see cFIREsim)

Interesting question. The relationship is exponential, because compound interest will speed things up near the end. i.e.: if you have half of your required stash already, you are more than halfway there in time.

A handy calculator would be nice. Any volunteers ? ;)

We are half way there with a SR of ~50%, soon to be ~75%

Great post as usual!

It isn’t necessarily exponential. Your investments could be at 24x annual spending in early 2008, for example

50-75% is awesome! Congrats

I am a big follower of Fi and doing well however one area of concern is the age gap between my wife and I. I’m 40 she is 21. Any way to adjust the 4% rule, or some tips for our situation. I am unable to find any FIRE blogs addressing this.

Plan for the youngest person – you aren’t FI until both are FI

The Mad Fientist has one. It’s his FI Laboratory.

Here is my favorite one… http://financialmentor.com/calculator/best-retirement-calculator

This one might help: http://mustachecalc.com/#/calcs/time-to-fi

Thank you!

What’s ironic is that the same periods during which accumulation took the longest also tend to be the periods during which the least accumulation was needed to fund an equal retirement (looking at this post side by side with your Endowment Fund post makes this easy to see). If only foresight were 20/20 too!

Very astute observation! There may or may not be a future post where I attempt to tie these together. There may be an useful crystal ball as well.

Generally speaking it appears that if you face a severe headwind while accumulating, a tail wind isn’t too far behind. And vice versa. Market cycles perhaps

Yep. The problem is that it’s psychologically easier (for me, at least) to fight off the nagging back-of-mind “what if this time is different?” concerns when trying to justify reliance on low WRs in the face of an overheated market than when trying to justify reliance on high WRs in the face of an underheated market.

I’m right there with you

I took a stab at it.

http://forum.mrmoneymustache.com/welcome-to-the-forum/cfiresim-spanning-earning-years/

Thanks for the in depth analysis! Currently I’m in my first full calendar year of being in the FI mindset. I’m tracking to finish the year with over a 40% after-tax savings rate. I assume this will increase every year as I get smarter with expenses, and get raises. So although I may “only” be starting with a 40% after-tax savings rate, it is by no means static and hopefully will jump by at least 5% a year. Conservatively speaking (hopefully conservatively), I’ve calculated that I’m about 11 years out.

I’ve enjoyed all your material thus far, but these types of posts were what got me subscribed (and hooked!). Awesome stuff, keep em comin!

Sweet, thanks JT!

I’ve been sleep deprived for the last 6 months so these posts are much harder to write. Math is hard

I am 25, and after doing my math, i realised ican retire before 40.

6 more years for me. I am just getting to the point that investments returns are starting to move the pile more than the deposits, but I like having both pushing it up.

If my wife goes back to work, that drops by a year or two. If we have a third kid, it could increase by a year or so. Things can change quickly!

I hear kids are expensive ;)

It is a great feeling when investments move the needle by a lot more than the paycheck.

We don’t make a lot initially, but we’re getting close to that 50% savings rate. Hopefully we can increase that now that we’re totally on board with the FI goal! I’m glad you set out all the math to prove your side. You guys have done awesome and even with all the math in front of them, haters still gonna hate.

This is a great article. GCC – you have inspired my wife and I to strive for early retirement and live the “slow-travel” lifestyle. We have been saving since our first paychecks for the last 6 years, but unfortunately at a “average” rate, maybe around 10-15% of our income. We recently made some huge changes in our life to help us achieve our goals and are now closer to 30%, looking to increase to 50% and beyond in the future. Articles like this make it seem possible and provide a logical path forward. I can’t thank you enough!

Awesome, thanks Kyle! You guys are doing great

This post comes very timely as I just finished a piece also re-enforcing that your savings rate is the most important variable in your control to build wealth in the fast time possible. Although it won’t get published for about a month, I will be sure to link back to this post.

Actually I just added the link as “further reading.”

Great post as usual!!!

Do you calculate savings rate after taxes or before taxes???

+1. Could use a bit more precision in how you calculate savings rate for this particular (excellent) analysis, as there are several methods out there.

Hi Markola

It is a simple version of (Savings) / (Gross income – taxes)

See my reply to Tyler below for a more in depth answer

I believe he is using after tax savings rates. In the post he says:

“Savings Rate – What percentage of after-tax income is spent and thus gone forever?”

and

“Below I evaluate savings rates of 25% – 75% of after-tax income, . . .”

I have this same never ending conversation with friends and family.

The revolving answer I give is “Its what you keep”.

Train, work hard and get a good paying source of employment that you can see yourself hacking out for >10 yrs.

Work hard, take responsibility for your actions etc, nobody owes you anything in life.

Cut back on every unnecessary expense and figure out how much you need a month to be content in life.

Invest everything else.

Then after all of that they look at me, but how much do I need???

Haha, I’ve had that conversation once or twice ;)

I’ve settled on 25x as the standard answer

That is a pretty nice way to look at things. In the accumulation phase, it seems like high savings are extremely helpful (even more than what you invest in – bonds or stocks). When you also invest the money wisely through tax-deferred accounts, you are doing yourself a big favor.

It looks like a person saving 75% of income can afford to retire in something like 10 years. It also seems like the worst case at a 3% withdrawal rate is working for 13 years.

Yeah, I’ve often thought about re-jiggering cFIREsim to add in a “how many years until retirement” option. The problem, from a design standpoint, is basically to identify pre-retirement items and post-retirement items.

If it were as simple as “how much am I saving each year, how much do I spend each year, and how much do I start with”, then I could easily implement something. Might have to be a separate page to not clutter up the already ridiculous interface. :)

Now that cFIREsim is open source, maybe a kind-hearted fan will implement this feature for the community :)

ps: I love the new look and feel

We are already there but took a bit of a different path that most others, we built and sold a company instead of living an extremely frugal lifestyle. Now the trick is to stay within that 4% SWR to keep from outliving our nest egg :).

Successful entrepreneurship for the win

Hey Jeremy – when calculating your savings %, what goes into (and gets excluded from) your denominator? I assume you the formula is Total dollars saved (including 401k + match) / gross pay (less taxes & health insurance). Is that correct?

And how does a mortgage payment get factored in? I currently rent, but am ready to purchase a home. Since mortgage payments are going towards an asset, does that get factored into your savings percentage? This is a gray area to me since this isn’t money spent and lost lost forever, but it’s not a traditional savings either.

Thanks!

edit: shorter answer

Hi Tyler

For the purpose of this post, I calculated it in the simplest way possible:

Savings Rate = (savings)/(gross – tax)

But at the end of the day, the goal is not savings rate but accumulated assets of 25x+ total spending. Savings rate is just a guide, and being precise with the math doesn’t change how many dollars you save or your rate of return. In short: use whatever method you like best as a benchmark and be consistent.

If you decide to buy a house, you’ll replace your monthly rent payment with a mortgage, property taxes, insurance, and maintenance. At some point in the future you may pay off the mortgage

At that point your balance sheet you will have an asset (a paid for house) and a liability (imputed rent.) These effectively cancel each other out, net zero. For this reason, I would personally account for the mortgage separately, and then calculate savings rate as something like:

Savings Rate = (Savings)/(Savings + Projected Retirement Spending)

Cheers

Jeremy

Fantastic analysis, I really appreciate the detail you went into there. I’m a 75%’er myself at the moment, so my day of freedom is coming fast. I’m one of those aiming for either a 3% or better draw down rate, or a more lavish ER than working life (lots of traveling, maybe life on a sail boat), so I’ll just keep filling my stockings for as long as I can tolerate the work environment.

As a member of the 75% club, getting to less than a 3% wr is almost too easy

Congrats! Sailing is in our future as well

https://gocurrycracker.com/want-sail-around-world/

Great analysis. My wife and I are saving 50% on one income. That being said, I’m thinking of ditching my job in a couple years and starting my own business. That will have the immediate effect of lowering my savings rate, but increase the chances of making a lot more money in the long term. And I feel confident I’d be happier whether or not the business is extremely successful.

At the end of the blog, it says Taxes are a constant percentage of total income. Investments are inside a tax sheltered account…I do’t belive you can spend out of a tax shelter account like IRAs and 401ks.??

Any thoughts into doing a post on de-cummulation strategies?

Great post as always! Puts to shame 99.9% of the crap out there

Great post. We’re about 2 years away from FI and 3 from early retirement. We’re no longer investing our non-retirement funds in the market since we’re creating our cash cushion but still continue to max out our 401(k)s until the end.

Great visual. Our savings rate is currently 50%, but will go down sharply in next several years. Hoping the savings we are making now will help us FIRE someday!

Very cool! But I don’t quite get the ‘income is constant.’

That is unrealistic, especially for a fairly young person who is just starting out working.

If your first job is for $40K a year and ten years later you are making $100k and you save 50% every year, then what you are aiming for might be 25 * 50% * $100k.

I know that’s pretty hard to represent in simple examples, and hard to encapsulate in a rule. But I think it would be nice to use a growth rate for income (or more likely a curve).

But it seems fair to encourage people to work hard to increase income, because even in a short career, the last few years could contribute a proportionally large amount, and also this would shorten the time required to add a buffer (i.e. go from 25x to 33x or whatever).

Thanks for the post!

Those would all be fine ways to go about doing the analysis. People are all at different stages of career and savings; young people can probably expect to grow income faster than inflation, people in their 40’s… maybe not.

Not everybody would inflate their lifestyle from $20k to $50k/year spending over a decade just because income grew, although many do. Another perfectly reasonable conclusion would be to continue spending $20k and grow savings rate to 80%, or to inflate BOTH lifestyle and savings.

I ultimately chose the method I did because it was the mirror image of the 4% rule’s constant withdrawal (which is also unrealistic.) Such is the way with simplification

Another great article! I’ve been doing a lot of research into investing but I’m still unsure of some things. Getting started is very nerve wracking! Especially when choosing a brokerage. It feels akin to choosing a wife before even having your first date! Haha. Anyways…

Just a background of my financial situation. It might make things easier for explanation. Also, for the sake of simplicity, we will “start” this scenario on January 1st:

I am making in gross 58k per year and plan to max out my employer 457 for $18,000 (No match, but there is a pension). Now, I am wondering what is best to do from here. Do I invest the remainder of my cash after spending (bills, food, etc) into a brokerage account (Vanguard/Betterment)? Or try to max out my employer’s IRA offering as well? And then invest the remaining cash in a brokerage? By putting so much money into my 457 and IRA, isn’t that money tied up until I become of age (I’m 28)? How could I retire early in this case and how would I increase my income through capital gains and dividends?

Also, I would like to learn more on tax savings through traditional to Roth IRA conversation. Are there any recommended resources (preferably free) that explain this process in a really dumbed down manner? I’m a civil engineer and much of this legal finance language goes over my head haha.

I’d greatly appreciate any advice anyone can give.

Thanks for your time!

If you haven’t done so already, you should read the stock series by Jim Collins. See here: http://jlcollinsnh.com/stock-series/

If you want to get into tax strategies, start here: http://www.madfientist.com/archives/

Of course, this blog also has top-shelf material that should be reviewed as well.

Good luck!

I echo Prob8’s recommendations

For a read world example of a Traditional to Roth IRA Conversion ladder, we are attempting to build the world’s longest (34 years.)

Nice visuals GCC. For the average person, the savings rate really is the key.

Which then makes you above average ;)

New to your site (love it btw) and first time poster here. So as a recent early retiree myself I have a couple of questions with regards to once you are “over the hump” so to speak. So if you are in the 2% range of swr to cover your annual expenses, why wouldn’t you lessen the potential volatility/risk? In another post it was mentioned that the biggest determining factor in the success is the first 10 years…so if my withdraw rate is already great with respect to my money lasting, why not lessen the risk especially with values in the market being currently on the higher side historically speaking? Of course I am giving up potential huge gains in the future, but if you aren’t planning to inflate your retirement lifestyle why risk it other than to leave a huge pile to charity when you are gone?

Welcome

I’m in agreement with Charlie Munger that “using [a stock’s] volatility as a measure of risk is nuts.” The two are not the same.

I sleep very well at night with a high percentage of equities in our portfolio. If another person doesn’t, has a 2% withdrawal rate, and would sleep better with more bonds, I wouldn’t argue

How do you go about taking distributions from a 401(k) without getting hit with penalties if you retire in your 40s?

A Roth IRA Conversion Ladder or 72t withdrawals

See this as an example:

https://gocurrycracker.com/gcc-vs-rmd/

I love your posts! It’s a true inspiration and exactly what I’ve been looking and aiming for:) Good luck in the New Year.

Great reading thanks. I thought I would share with you our situation….and although not completely free, we have found a solution until we are.

Since 2009 we have been house and pet sitting for friends, this was a great way for us to get some space and quiet, it also introduced our three girls to increased independence.

We are in our mid-forties the kids (3 daughters) have left home and we old our house in December 2015.

We run a business and it being only 4 years old a lot of our money is still tied up in it…..however we are debt free and look forward to the business paying us back.

Anyway, to cut a long story sort, we are using the advantage of being able to work remotely, I think the new term of phrase is Digital Nomad. We decided it was time for an adventure, you never know what might happen and there is no guarantee we will make it to retirement age.

So, in June we board a flight with our one-way tickets to experience a different language and culture, we have already secured 3 house sits in southern Spain totaling 5 months…..let the adventure begin.

House/Pet Sitting – We provide a free live in minding service in exchange of free accommodation and utilities.

Mike and I are originally from the UK but have lived in NZ for the past 15 years.

It’s a great blog and a audience here great. Thanks for doing it. A question I had is if our target retirement income is $40K/annually, is there an easy way (i.e. a formula) to calculate how much we would need to save each year in order to retire in 10 years? So basically I’m looking for a reverse calculation. I think 50% of income or any other relative number makes it a bit harder as everybody’s income is different (and also different $ CAD vs USD). I really appreciate your answer.

Everybody’s income is different, which is precisely why percentages are used here.

From the data shown in this post, a savings rate of 75% invested 75% in stocks has a mean time to FI of 8 years. Implied in the savings percentage is that you are spending the rest. So for $40k/year in retirement (25% spent), you would need to save 3x that (75% saved) for 8 years +/-.

Also see this post.

Did I read that correctly? You were depositing 100% of your paycheck into a brokerage account at the end? I assume you were living off dividends? If so, why not reinvest those and pull your expenses out of your paycheck? I feel like I’m missing a tax-code hack.

Money is fungible, so you can choose to look at it either way.

A little tired of seeing this crappy math where if you save 75% of your income you can live with 25% only….I and most of us don’t wanna live on 25% of current income in $ forever…we want to be able to spend more at FIRE than now and live better not struggling all our lives…this simple assumption is really silly in my opinion….

Are you saying, “I don’t want to live like I’m poor forever.”

Crappy math sucks, I agree. Although we saved 75% of our income and now spend more in FIRE and live “better.”

Cheers

Should be around 6 years I’m hoping! I’m 22 and trying to get an early start on this by saving around 70% of income. People look at me and are like “you can’t retire that early” and I’m excited to prove them wrong! Many people can’t understand why I would want to retire that early and I can’t see why they wouldn’t want to.

I was asked the other day what my dream position at my company would be and I responded “retired” 😂

Just ran across your blog a few months ago. Love it. Found this post bc I was searching for more details on your savings rate. I’m always confused when someone talks about their savings rate on forums; are they generally using gross or net income? I see you use net. I’m having a little trouble calculating mine. These are my monthly numbers.

Gross: 6412

After taxes: 5154

After taxes and all other payroll deductions (this is the number show as net pay on my statement): 3400

Savings: (401(k), ESA, HSA): 1847

Is my savings rate 29%, 36%, or 54%?

It’s a weak metric – there are a lot of assumptions. I’d say your savings rate is about 36%, maybe more, maybe less.

3 of the big assumptions in this post’s math are

– earnings/spending are constant over the entire savings period

– pre-retirement spending = post-retirement spending.

– current savings = 0

Change any of those and the time to FI changes (perhaps substantially.)

This earlier comment may be of interest:

Makes sense, thank you for the prompt reply! I’m going to try to get super aggressive with my savings and hopefully be close to my number (~1.25 million) in the next 10 yrs. I have been saving primarily in Roth for over 10 yrs. Mainly due to following Dave Ramsey’s advice. His target audience is mainly poor people, and I guess his philosophy is that if you follow his path, you’ll retire wealthy and definitely be in a higher tax bracket. Anyway, I can see the flaws.

I switched to all pre-tax contributions and bumped up the percentage. That should give me a nice boost in savings rate without *too* much pain hopefully.