Welcome to the First Official Go Curry Cracker Financial Review! In a series of new posts, I will review the financial situation of an anonymous reader, and provide actionable recommendations

Welcome to the First Official Go Curry Cracker Financial Review! In a series of new posts, I will review the financial situation of an anonymous reader, and provide actionable recommendations

The lucky winner of our Financial Review goes to reader Bob. We exchanged many emails over the holidays, and put together a great plan that will help Bob and his wife overcome their financial concerns, retire earlier, and save $1.5 million or more in taxes

Along the way we learn about RMDs, and the sweet deal that Federal employees have in terms of pension and health benefits

Hey Jeremy and Winnie

Love your site! My wife and I have been talking about ER for some time now but are scared to death of running out of money and are worried we haven’t saved enough. Your tax-free approach is a different take of which you don’t hear a lot of folks talking about. I just turned 57 and she is 54. Getting a little freaked out about retiring at this age. ;)

I’m already thinking on how to move investments tax efficiently to get out of the tax trap.

Here is our financial situation:

We have our main home, a rental property, and a condo in Texas. We plan to sell the rental property and use the proceeds to pay off our mortgage. The condo is already paid for

We have the following investments:

725K 401k

1.1M TSP

250K Roth IRA

500K taxable brokerage account

72k private equity investment at 7.5% yieldMy wife will also be eligible for a pension as long as she works until age 56, her Minimum Retirement Age, which she can start drawing from at age 60. My early SS and her pension would provide an equal income, totaling ~$4,300/month. She would also be eligible for SS starting at age 62, and for Federal Health Insurance coverage starting at age 60. We currently pay a total of $612/month for coverage for both of us, which includes our HSA contributions.

Our current thinking is for both of us to work until the end of 2016. I’m earning 95k/year and my wife is earning 75k/year, totaling 170k a year. We both max out our 401k/TSP and also contribute to our ROTH IRAs.

My question is how would we be able to get the deferred 401k and TSP money converted to the Roth IRA in the most tax efficient manner? I understand about drawing down the taxable account but concerned about the RMD at 70. If it would work, we could hold off on the SS and the government pension in order to get this converted, as SS would be ordinary income? What are you thoughts with the 4% living rate?

When we retire, we would like to hit the road traveling and spent our winters at our condo in Texas. We estimate we will spend 48k a year. We’ve always been pretty frugal on the things we buy, as big houses and expensive cars don’t really do it for us. We also don’t have any children to inherit our assets

The photos you’ve posted are great. I check out all of them. Keep up the great photos and thanks for your assistance in helping everyone get out of the rat race early.

Bob

Anywhere, USA

Hi Bob

I have some good news and some bad news.

The good news is: The only people in the country more financially able to retire TODAY have last names that sound like Kennedy, Rockefeller, and Getty. Congratulations!

Any way you look at it, you are ridiculously wealthy. In fact, you and your wife have been financially independent for at least 10 years. While it is certainly normal to feel some concern about the paychecks stopping, the bigger concern at this point should be making sure you aren’t wasting your life working when you could be pursuing your passions

The bad news is because you have saved such a substantial portfolio, you are going to pay tax. Lots and lots of tax

Still, I will suggest some ideas that will save you $750,000 – $1.5 million in tax over the coming years

Let’s get started

Financial Summary

Let’s look at your total financial picture

Total invested assets: $2.65 million

Homes: Main home and condo, no mortgage

Monthly Pension and SS: $4,300($51.6k/yr)

Wife’s SS: $26k/yr (estimate, not included in analysis)

Monthly spending in retirement: $4,000 ($48k/yr)

You expressed some concern about the 4% Rule, but you have so much income and assets that we don’t even need to consider it. Your target withdrawal rate is actually 0% (!), as the Federal Pension and Social Security will cover 100% of your expenses.

There are a few ways to look at your current financial options:

- Spend $48k/year with 0% withdrawal rate. Pension and SS cover all expenses

- Spend up to $157k/year, 3x your current plan – 4% Rule allows for this level of spending

- Spend up to $237k/year, living like a Rock Star for a few years (7% withdrawal rate) Since Pension and SS support 100% of your target lifestyle, you can take risks

Any fear of not having saved enough has no basis in reality

Value of Working 2 More Years

Your plan of working until the end of 2016 is based on the idea of reaching the Minimum Retirement Age (for your wife, 56) for the federal government pension (FERS)

But what happens if your wife quits today, at age 54?

Since I’ve never participated in these plans, I had to do a bit of reading. This is what I determined (See Jane’s example)

With over 5 years of qualifying service, your wife qualifies for a FERS Deferred Retirement. By retiring 2 years before the MRA, the pension payments are reduced AND she is ineligible to participate in the Federal Employee Health Benefits. You also forgo 2 years of income and some small incremental SS benefits

These sound like bad things, but remember: You don’t need any more money. But let’s be objective, and use cold hard reason and logic to determine the actual financial value of that time

Value of Pension

The formula for determining the FERS monthly annuity value is as follows:

High-3 Average Salary x Years of Service x 1% = Payout at Age 62 (Estimated $2,300/mo)

Since your wife has already saved $1.1 million in her TSP, she must have worked for the government for quite some time. I am going to assume 20 years since I don’t know exactly. In this case, working 2 more years would increase the payout by 10%. Assuming that the final 3 working years are the highest income years, with annual raises of 3%, the High 3 average would also increase by 2-3%

The net impact to the payout for 2 years of work comes to about 12%. Your expected payout of $2,300/month would be reduced to $2,024, a reduction of $276 monthly

Is it worth working 2 years to received $276/month? What if instead we purchased an inflation-adjusted annuity with spousal survivor benefits for the same income?

Present value of that annuity (2015) is about $82,000

Value of Health Benefits

By retiring 2 years earlier, your wife loses eligibility to participate in the Federal Employees Health Benefits

This needs to be compared to what could be purchased on the open market

Coverage between Government Group Health Plans and a Silver level family plan purchased through Healthcare.gov seem similar (my opinion), with minor co-pays and Out of Pocket costs of ~$8k year max. On Healthcare.gov, plans cost about $1k/month. Through the FEHB, plans cost $462/month

That is an incredible $538/month savings! This is because the Federal Government continues to pay 72% of the cost of insurance after retirement, something unheard of in the private economy

As we did for the annuity, we can translate this into present value. An annuity with $538/month payout would cost $160k (and perhaps more as health insurance costs have been rising faster than inflation)

Conclusions

For 2 years of your wife’s time, she would receive:

150k in additional income (pre-tax) (After tax: ~$90k)

An annuity worth $82k

A lifetime health insurance subsidy worth $160k

A small increase in Social Security benefit (ignored here)

This looks like a great income, roughly $165k/year after tax for a total of $330k. This is equivalent to ~10% of your net worth (excluding pension and SS)

The Retirement Years

Whether you retire today, in early 2015 (age 57 and 54), or work 2 more years until the end of 2016, there is a period of years before Social Security and Pension payments begin

What is the best way to pay for your cost of living during that time, which accounts should the money be withdrawn from, and how do we pay the least possible amount of tax?

Bridging the gap

Most people are aware of the 10% penalty for early withdrawal from tax-deferred accounts. This is the stick the government uses to discourage you from using this money before retirement

For this reason, many people set aside funds in a taxable account or ROTH IRA to cover these years, to bridge the gap between no longer receiving a paycheck and eligibility for penalty free withdrawals from 401ks/IRAs or eligibility for Social Security

This works, of course, but there are better ways. There is one exception, referred to as Separation from Service, which states that if you separate from service from your employer during or after the year you reach 55 years of age, then you can make withdrawals from 401ks/TSPs without restriction and without penalty. This only applies to qualified plans like 401ks & TSPs, and DOES NOT APPLY to IRAs. If you rollover your 401k or TSP to an IRA, you lose this option

Since both you and your wife will be 55 or older in 2015, you both qualify for this exception, and this is what I recommend you do

For others in a similar situation but younger than 55, there are other methods to access tax-deferred funds penalty free, most notably Substantially Equal Periodic Payments and a ROTH IRA Ladder (what we do.) The Mad Fientist wrote a great guest post about this topic on Jim Collins’ site

Starting from day 1 of retirement, you should fund all of your annual expenses by withdrawals from your 401k and TSP

Minimizing Taxes

Your Tax Base

Currently, you live in a State with an income tax but have a condo in Texas. As soon as possible after retirement, you should change your tax base to Texas which has no tax on income of any kind

This will reduce your effective tax rate by up to 6%

Required Minimum Withdrawals

The government is very kind in providing options for decades of tax-deferred growth in our 401ks and TSPS. But tax-deferred is exactly that, deferred. Someday, you have to pay the IRS

As we start withdrawing funds from the 401k/TSP, we will pay tax. But this isn’t enough for the IRS. They want taxes on ALL of you deferred savings, and so they mandate Required Minimum Distributions starting at the age of 70.5. Jim Collins has a great RMD overview that is definitely worth reading

These minimum withdrawals increase with age, and can be substantial, resulting in tax rates of up to 39.6%. Even worse, because RMDs push us into higher tax brackets, qualified dividends and long-term capital gains become ineligible for the 0% tax rate and Social Security income becomes taxable

To minimize taxes, before RMDs are required at Age 70.5, we want to withdraw as much money as possible out of tax-deferred accounts while paying the least amount of tax

Our goal is to minimize total tax paid, and so we will choose to pay tax in the short term at 10% and 15% in order to avoid paying tax later at 25% to 39.6%

Between now and 2028, when you turn 70.5, you want to withdraw enough funds from the 401k and TSP to reach the upper limit of the 15% tax bracket, plus deductions

In 2014, for a married couple filing jointly with standard deductions and exemptions, this limit is $94,100. Any income from interest, dividends, pension, or social security will reduce the amount you can withdraw from the 401k/TSP, dollar for dollar

For this reason, we want to minimize other income sources. I would recommend delaying Social Security until after Age 70.5, and taking the Federal Pension at the latest date possible (I believe Age 62.)

Minimizing Taxes from RMD

There are 3 different tax situations you will face during retirement

- The Gap between Retirement before the Pension begins

- Receiving Pension payments but before RMDs

- Required Minimum Distributions

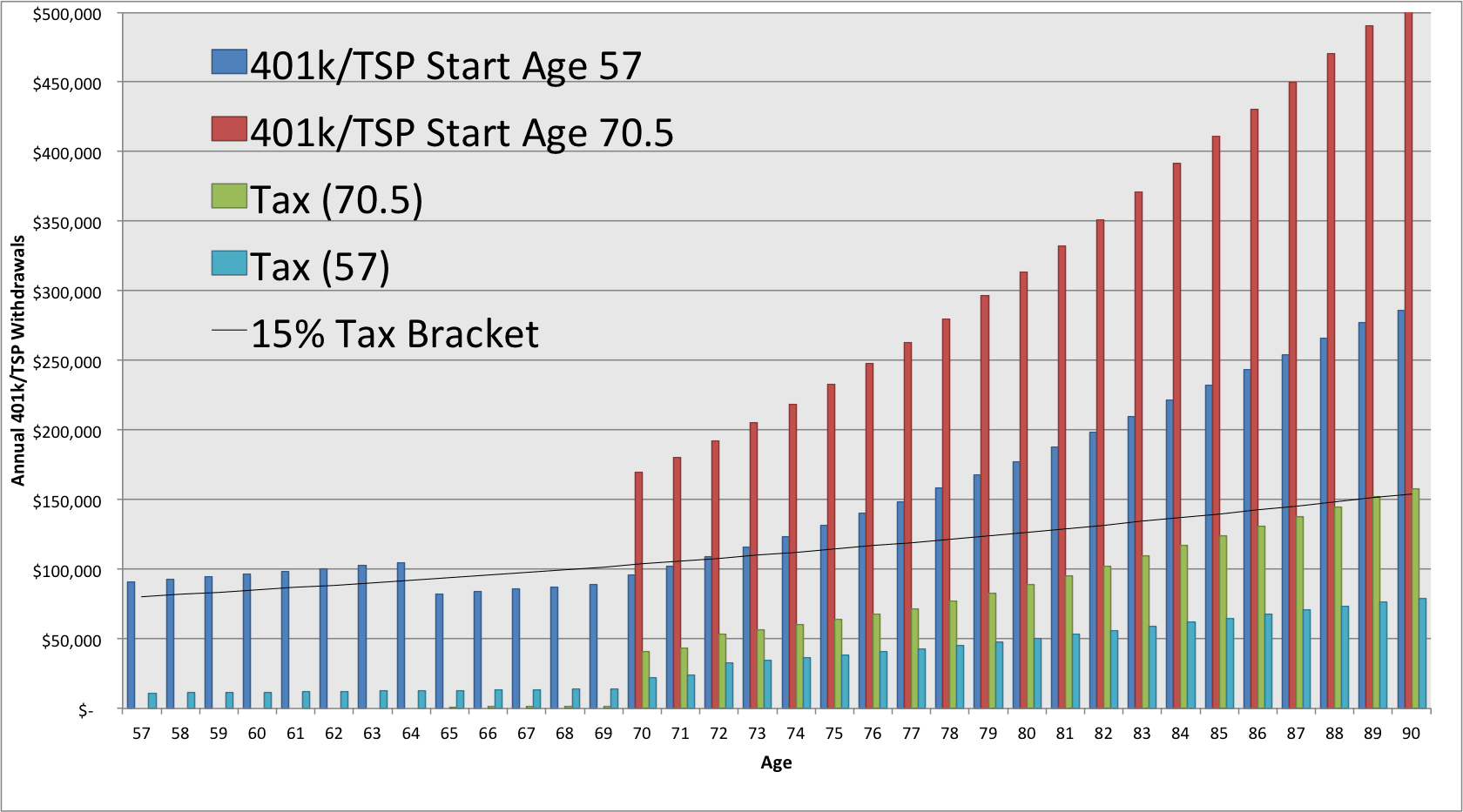

A picture is worth 1000 words, so here are some examples

These charts use Bob’s Age as the X-axis and Annual 401k/TSP withdrawals on the Y-axis. I’ve assumed 7% annual growth of 401k/TSP (probable) and tax brackets adjust with inflation of 2% (IRS inflates brackets slower than inflation to increase tax income)

Starting in 2015 at Age 57, withdraw funds to the max of the 15% tax bracket. Because other income is low, the Standard Deduction and Personal Exemptions allow us to withdraw a bit more.

One your wife’s pension starts at Bob’s Age 65 (Wife’s Age 62), reduce 401k/TSP withdrawals by an amount equal to the pension payments

At Age 70.5, RMDs begin. In the early years, the 15% tax bracket is greater than the RMD, but over time the RMD grows faster. Any funds withdrawn from the 401k/TSP before Age 70.5 that are not spent on consumption, Convert into your ROTH IRA, which will allow those funds to continue to grow tax free

If instead you were to fund the early years from the taxable account, you would pay minimal taxes in the years before RMDs begin. This would allow more tax-deferred growth, at the cost of greater taxes later

If instead you were to fund the early years from the taxable account, you would pay minimal taxes in the years before RMDs begin. This would allow more tax-deferred growth, at the cost of greater taxes later

To compare the two, we can look at both situations on the same chart

To compare the two, we can look at both situations on the same chart

By paying tax at 10% and 15% in the years prior to Age 70.5, tax bills in the later years are reduced.

By paying tax at 10% and 15% in the years prior to Age 70.5, tax bills in the later years are reduced.

The total delta in tax between today and age 90 is ~$750,000. By drawing down the 401k/TSP in the earlier years, you eliminate $750,000 in tax! And if we look out to Age 100, this method saves over $1.5 million!

Sounds impressive, doesn’t it? Even so, you will still pay up to $2 million dollars in tax by Age 100

Present Value of Future Tax Payments

These sound like big numbers and big savings. Let’s look at the cost of those future taxes today, in 2015, similar to how we determined the value of working two more years

The NPV of all future tax payments to Age 90 is about $300k, roughly equal to the value of working 2 more years.

That $750k future tax savings? About $60k in 2015

(Determined using NPV function in Excel, assuming 7% alternate investment option)

End of Life and Charitable Contributions

Even with several decades of living the dream, making substantial tax payments on the way, the value of your portfolio at Age 100 will still likely be in excess of $10 million.

Now wouldn’t be a bad time to think about what to do with that wealth, potentially even contributing to causes you believe in.

To minimize taxes, you can contribute funds to an endowment in the years with your highest tax burden (another Jim Collins classic.)

Conclusions

By all accounts, you are already financially independent and able to fund your desired lifestyle for the rest of your life. You no longer need to trade your time for money

You have the opportunity to increase your net worth by <10% via your wife’s pension and access to the government health plan. The cost is 2 years of life

According to the social security life expectancy calculator, you can expect to live another 28 years. Of course, not all of those years are equal. Is it worth trading 7% or more of your remaining life (2 years) to increase your net worth by ~10%?

Only you can determine if this is a good trade

By leaving your 401k/TSP with your employers, at least through the age of 59.5, you can withdraw funds penalty free beginning in 2015 or as soon as you retire. Using this to fund the gap years will minimize long term taxes

Were we in the same situation, I would quit work today and start traveling. Any additional income is unnecessary

Because of your strong concerns of insufficient savings, perhaps you quit today and your wife works 2 more years, assuming she is agreeable. It is hard to predict the future of health insurance costs, but many believe it will increase faster than inflation. A guaranteed lifetime subsidy on health insurance would be hard to turn down.

During these years, and the first several years of retirement, I would use a tool like Personal Capital to track expenses like a hawk. By seeing income exceed expenses, and watching net worth continue to grow despite withdrawals, will help minimize any fear of not having saved enough

To minimize taxes, I would move to Texas as soon as convenient, and otherwise follow the plan outlined above.

Good luck, and may you mock the longevity tables

Update: A follow up was posted 5 years after the Bobs retired. Check out the rest of the story: Scared to Death of Early Retirement, No More. An Update.

————————————————————————-

Are you interested in having your own GCC Financial Review? If you have a unique or interesting situation that can provide a good example or lessons learned, please submit your application via the Contact form

On the open market you might pay thousands of dollars for this level of financial feedback, but here on Go Curry Cracker, the price is an incredibly low $0!

As a random guy on the Internet, this is the actual value of the recommendations I provide :) This is for entertainment purposes only. Always consult a professional.

Are you also a random guy on the Internet that has some suggestions or ideas to offer? What would you do in Bob’s situation? Please share them in the comments

Great analysis!

One detail that might make a difference in Bob’s situation is that it’s likely that he and his wife may have more than 30 years of service at retirement, enabling them to receive pension benefits immediately. I font think there’s any downside to this (I.e., no increased benefits by deferring). I believe the overall strategy you’ve outlined would remain the same.

I’m in the same boat with a few more years to the MRA and a few less dollars.

Thanks Kendall. This is my first time looking into FERS and FEHB. It is good to know that it isn’t just the IRS that likes to write confusing documentation :)

Any and all expertise, suggestions, and corrections are welcome

Wowsers. I’m sure it’s harder when it’s your own money and your own future, but it seems like a pretty cut and dry “you’re good to retire” situation to me!

If you have over $2M in invested assets, plus a pension&social security, you can retire right away. Of course, I am not sure what the couples expenses are per year.

If one is not sure about retirement even with that kind of financial security however, then the issue is probably something else. Or maybe it is the hedonic treadmill where $1M is the goal, but when reached looks like not enough, so you strive for $2M, which when reached looks like not enough, so you strive for more…

Enough’s never enough in that case.

I think they plan on spending ~50k per year.

Just imagine, even if they withdrew it now, that’s still 40 years. PLUS A PENSION.

To be eligible for the FEHB the employee must take an immediate reduced annuity at MRA, in this case age 56. Deferring the pension ends your participation in the FEHB and precludes you from re-enrolling. Clearly, these folks are sitting pretty and the resulting reduced annuity only alters the income calculation for them slightly.

From: http://www.opm.gov/retirement-services/fers-information/types-of-retirement/#url=Insurance

“If you receive a deferred annuity, you are not eligible to continue any health benefits or life insurance coverage you had while employed.”

This is true, although if they have 30+ years the annuity won’t be reduced, either.

Joe, thanks for the feedback. The wife will able to “postpone”, not defer, her FERS pension until she is 60 and still be eligible for the FEHB because she will have met her MRA of 56 AND have 20+ yrs at the Fed. She was born at the end of 1959 and meets the “years of service” criteria for the special case from what we’ve read. http://bit.ly/1xiFF61

Thank you very much for doing this analysis. Keep them coming. I am 44 (today) with a good amount of savings and I am slowly learning more about this topic for when the time comes for FI.

After publishing this post, I’ve received quite a number of requests. More will come!

Great post, situation and analysis, Jeremy!

After reading the title, I literally burst out laughing when I started reading the list of assets. These folks are there and then some. ;)

This is a situation very similar to several I’ve encountered during my one-on-one sessions at our Chautauquas: People who have been very diligent in their saving and investing, and modest in their lifestyle; who find themselves well into FI without fully realizing it. It is always a pleasure to be able to confirm for them – for on at least some level they already know – that, yes, you are there!

I think your advice is spot on. If I might offer a couple of additional thoughts to compliment yours:

I loved your analysis of Mrs. Bob’s last two years of working. Certainly, she doesn’t have to. But my guess is, given her psychology that has helped get them to this impressive point, it will be very difficult to walk away from those goodies. Certainly she should if she hates her job. But, if it were me, I’d find it very uncomfortable to do so. If she feels the same, no harm in staying.

2. I love your suggestion that they boost their withdrawal rate to ~7% and live the “rockstar life” for the first few years. This they can easily afford, especially as they have no heirs. As to how many years, they can monitor their investment performance and let that be their guide.

My only caution would be to keep this spending for isolated stuff: Travel, cash-bought cars and the like. Be careful not to get into things that have big on-going expenses locked in. Big houses and yachts, for instance.

3. Speaking of heirs, I also agree they should start thinking about what to do with their money once the time comes. Assuming they live to a ripe old age, your estimate of 10m remaining is likely to be conservative. When most people look at the Trinity Study they focus on the rare times the 4% rule fails. What they miss is how often it results in vast fortunes left behind. Given the conservative spending Bob and his wife have planned, this is very likely to be the case for them.

One thing they might consider is a charitable gift annuity. Many, maybe most, charities offer these. Just like an annuity, you put up a lump sum of money and in return you get a guaranteed income for life. When you die, the charity gets what’s left. Here’s an example: http://nhpr.giftplans.org/index.php?cID=92

4. Since most 401Ks are saddled with high fees, the moment Bob retires (the 401K is Bob’s, right?) he should roll it into an IRA where he can place it in low-cost index funds. Vanguard would be my choice.

5. Since TSPs have great investment options and stunningly low costs, I’d hang on to this. In fact, I would spend down the 401K – even once rolled into an IRA – before touching the TSP.

But these are minor considerations to your already excellent plan. :)

Thanks Jim

I think your comment is spot on. Those of us that read and write financial blog posts everyday can forget that our understanding of this stuff is the exception, not the norm

Many people like Mr. and Mrs. Bob live frugally and end up quite successful financially, but there is a big gap between thinking you might be Financially Independent and knowing it

re: Moving Bob’s 401k to a Vanguard IRA

I think this is the right think to do, but not until Age 59.5. If he moves the 401k before then, he loses the option to make penalty free withdrawals under the Separation of Service clause. So I recommend leaving the 401k with the employer until then, as it is a more flexible and shorter term commitment than setting up a SEPP

That said, it would be good to look use something like Personal Capital’s 401k Analyzer to make sure the man isn’t sticking it to you

And thank you for clarifying what it means to live like a Rock Star for a few years. We want to end up like the Rock Star that fades away with a healthy brokerage account and a steady royalty stream, not the rock star that ends up broke and living in his Mom’s basement. So this means a few years of taking luxury cruises, 5-star accommodations while traveling through Europe, and business class flights, not taking out a mortgage to buy a private island

Thanks Jim!

Jeremy

D’oh!

Of course you are right about leaving the 401k in place until 59.5.

As you explained in your post…

Jeremy. I’ve enjoyed your blog immensely. Im in the process of planning my early retirement and thought, with your scenario, I had it all figured out. I called my companies 401K provider and talked about qualifying for the age 55 penalty free withdrawals. They informed me that my company doesn’t allow it. Only one wirhdrawal allowed. My choice is to take it all at once out of the company 401K( they recommended rolling it all or most into an IRA… Of course) or leave it all in. It literally blew my plan apart.

We are in a similar situation to you. We have two under 3 children and its a concern for early retirement that no one online addresses and we live internationally. We left Taipei in February and cried when we had to!

What options do we have?

Hi Mike

Don’t worry, there are other methods. There is a link in the post above to a post on Jim Collins’ site about early 401k withdrawals that would be good for you to read

What you would probably end up doing is setting up a series of Substantially Equal Periodic Payments. https://personal.vanguard.com/pdf/s164.pdf

Essentially you have a contract with the IRS that you will take out a specific sum of money every year until you reach Age 59.5, or 5 years, whichever is longer

Bank Rate has a decent calculator for determining withdrawal amounts

The SEPP method isn’t the most flexible option in the world, but it is better than paying a 10% penalty

Cheers

Jeremy

First off, I want to publicly thank Jeremy for taking the time to put this all together and giving us the opportunity to be the first Financial Review. I was shocked by the results and the amount of time he must have put into it. It’s much appreciated, don’t doubt it.

Jim, thanks for your input and support. Your site http://jlcollinsnh.com, like Jeremy’s GCC, is at the top of my early retirement bookmark list. I refer back to it often. Others I review are Mad Fientist and MMM.

Both of you are correct. It is difficult to get our heads around the options that are now available to us. When you both said, Live Like A Rockstar, it will be a difficult task to accomplish. I think the Rockstar life will be something like buying a used medium sized RV and traveling the country for a few years while wintering in Texas. We’ve never been big spenders and are still surprised on how this added up as well as it did. We’ve talked and I will call it a day at the end of this year. The attitude adjustment at work has already begun. For 10 months more, Mrs. Bob will be able to get us both back on the Federal Health plan in 4 years but to do this, she may be forced to take her FERS annuity.

We appreciate all the great comments in the posts and will continue to review as they come in. Keep up the great work and continuing to help others realize their early retirement possibilities.

Hi Bob…

I’m honored to hear it, and in GCC, MF and MMM you’ve name three of my top picks as well.

I hear you on the “rockstar” life. My wife and I are also at this point and, like you, we just don’t have the interest in stepping up our spending. While flying in coach is an absolute misery for me, she still can’t get me to give the rascals the money for 1st class. So I grimily and grimly tough it out, gloating over the savings I don’t need. Sigh. :)

You really are destined to leave a ton of money behind, so do give that some serious thought.

Hope you keep us all posted on your journey and If you make your way to NH let me know. I’ll buy the coffee. Yes, I know you can afford it. ;)

Will it be Ecuadorian Above the Clouds coffee?

Not unless I can score some more. I burned thru my supply in about a week. :)

It is a very small farm and crop. :(

It is my pleasure, Bob (and Mrs Bob)

I think many people can learn from your example, and it gave me the motivation to finally do the RMD analysis I had on the back burner

It may not feel natural to go into full Rock Star mode, and that is OK. But knowing your could if you wanted to is a helpful thing. At this point, there is nothing to fear except running out of time and health. You are in great financial shape.

RV’ing around the US is also on our list. Maybe we’ll pass through Texas one winter

Good luck to you both!

The door will always be open. Would be great to meet you guys face to face sometime while crossing paths.

We’ll buy the coffee for you and Winnie (no coffee for GCCJr). Jim is for sure buying ours. :)

Bob, it was fun reading your situation and how you and Mrs Bob are viewing your current situation. Much like yourselves I found it difficult to pull the plug (the wife was able to retired from her government job at 56), but an old sports injury hastened that day when I turned 60 (almost seven years now). Our assets at the time may have been slightly higher than yours, but except for the wife’s small government pension, SS would be everything else coming in outside of investment returns. Let me give you an idea of how the last seven years went since we are similar in many ways:

-Probably like you guys will do, we did not increase our spending since we moved to a low cost state a few years before I retired (not TX, but even a cheaper COL), had already invested in our future vacationing with a large # of timeshare points (we travel 4-5 months out of the year), and we are comfortable with our lifestyle in general.

-I still enjoy finding ways to cut down on expenses that don’t involve draconian changes to our lives. That involves examples like changing to lower cost streaming media services, cell phone service, and so on. By doing so our yearly expenses have actually dropped over the last seven years with no lowering of lifestyle. Much of that has to do with moving to a lower cost state like Jeremy recommended.

-I stay active in the markets but I stay in my comfortable swim lanes. That includes buying and selling stocks and ETFs, and selling covered call and put options (although I might dip into crypto currencies when the next serious downturn occurs). Even with a balanced portfolio including cash and bonds dragging down returns, we saw our bottom line go up north of 40% in 2020.

I’ll cut it off here with just an echoing of Jeremy’s point around the fact that you can both stop now. You are in great shape. Enjoy yourselves.

Mr/Mrs Bob

Congrats on doing so well.

I imagine that it might be difficult to shift gears but I do think you should take time to enjoy the results of all your hard work.

What a nice problem to have! Hope we could have this kind of worry when time comes. :) Congratulations, Bob!

What a nice post, Jeremy! I read it a few times. First time, I was in total admiration for Bob’s accomplishment; second time, I worked on the abbreviations; third time, I worked on the numbers. I am totally saving this post for future reference.

Wow if I had that amount of money I would be ecstatic. Great job Bob. Unbelievable analysis Jeremy. NOTE: one critique is that in my opinion these people are a slam dunk for ER, maybe on the next one do someone a bit further down the savings amount or someone with higher expenses. With their low expenses they are more than set!

Hi Mark

Ignoring exact numbers ($, age, etc…) we can learn many things from Mr and Mrs Bob’s example:

– To be a slam dunk for retirement, you need to be financially and emotionally ready. Both are required

– It is possible to withdraw funds from tax-deferred accounts in several ways before age 59.5

– If you use 401k funds to “bridge the gap” instead of $ in a taxable account, it can result in a lower tax bill

– the huge impact RMDs can have on taxes

– how to use cost of an annuity and net present value to see the true value of future income (working 2 more years, pension, health benefits) or expenses (taxes)

There will be more, and I’ll try to address many different circumstances, including examples with high cost of living. I’ve received quite a few requests

Cheers

Jeremy

Jeremy, you rock!

Hi Jeremy. Love your stuff! Thanks for your time and information. Do you ever offer advice for Canadian transplants? I’d love to be thrown in to the hat to have this analysis for my wife and I. We’re not even close to Bob’s situation but, I believe we’re on track. I tend to get overwhelmed by all the information out there and all the different opinions. I’m also extremely skeptical about getting advice from any old financial advisor. Anyway, in the meantime, I will keep reading with enthusiasm. Thanks!

Hi Jo, and thank you

Check out the RFR link on the Menu bar for submission guidelines. I’m not familiar at all with Canadian tax law, so can’t offer and suggestions there.

There are a lot of opinions out there, and information overload. Hopefully this site can help, you can get started here. There are also some great blogs on the Blogroll.

If you have questions about any post, I read every comment

Welcome!

I love this blog!! Great post, analysis & comments. I am, however, surprised that no one has mentioned the issue of long-term care as part of their overall ER plan. Does their federal health insurance cover LTC? If not, you may be assuming that given the sizable assets they have that it makes sense to self-insure, but if that’s the case it warrants mentioning and a brief analysis of the options. While they may be able to self-insure, they should at least consider buying some protection against that risk, since they can obviously afford the premiums. If they don’t like LTC insurance because of the issue of rising premiums, they can consider the costs/benefits of a linked-benefit LI policy. Assuming both of them are currently healthy enough to qualify for LTC insurance or a linked-benefit policy, this might be a good time to get in before a health issue comes up.

Hi Brad, it sounds like you’ve done this analysis before? Can you share more details?

I haven’t done the in-depth numerical analysis, because I can’t qualify for LTC insurance (I’ve already been rejected). I have been following what a lot of the financial advisers are saying… things like: a married couple has about a 70% chance that at least one of them will need LTC at some point, most health insurance plans do not cover LTC unless a separate policy or at least a rider is purchased, the current cost of LTC can be from $80k to well over $100k /year depending on what state you live in (obviously if you’re an expat & live in a country that provides quality care at low cost it’s a different issue), you should generally insure for 2-3 years of LTC, premiums are cheaper when you get the insurance in your 50s-60s (if you’re healthy) and the premium increases have to be done by/within pools and approved by the state insurance board, etc. Many major insurers are now getting out of the LTC business because they’re losing money, because the actuaries didn’t project accurately enough for increased longevity, and because LTC costs are rising faster than expected, so it’s getting even harder to find a policy & qualify. All of this is leading to what many in the field think will be an LTC crisis in the future, where states have to take on the burden (under medicaid) for huge numbers of aging boomers whose assets will be wiped out by LTC costs.

Because of all this I thought about getting LTC insurance when I was 52, but figured I’d do it in my late 50s. After all, I was healthy and had low risk factors for all major diseases. Then at 53 I had a “silent” heart attack and had to have emergency triple bypass surgery and valve repair. I had virtually no risk factors, other than a stressful job and a slightly high cholesterol level (215). Now I can’t get LTC insurance, and have to account for self insuring as part of my calculations. I retired at 56, but figure 300k of my current assets have to be set aside for LTC if it’s needed. So I use the remainder of my assets in calculating whether I’ll be ok financially, and just to increase the margin of safety I use a 3% rate of withdrawal instead of 4%.

I do strongly believe that anyone (living in the US) calculating their retirement number needs to consider self-insuring or paying premiums to insure for LTC costs. And no, I don’t work in the business and have no conflicts of interest in giving that advice.

I respect your intelligence and analytical abilities. If you look into this issue I’d love to read what your thoughts are.

I’m not sure I’m ready to dig into this yet. If I had LTC insurance, it would be the only kind of insurance I have…

Here in Taiwan, there are many Senior Citizens with full time live in care. This is often a younger person from the Philippines or Indonesia who has come to Taiwan to earn a good income, and they will do all shopping, cooking, help with all of the activities of daily living, etc… We often see them pushing wheelchairs in the park

That good income is about $800/month (plus meals and housing)

This person sounds like a fraidy-cat and they should just retire already. Late 50’s isn’t that young anyways plus they have saved enough. Should focus more on your health than your bank account if you ever plan to use even half of what he and his wife have saved.

Man…some people just waist they lives because of this mental holder that is living without working….

If I had 30% of what these guys have I wouldn’t be selling my time to anybody. I would rather be spending my time/money with things that really makes me happy and good…including volutear work

I suppose this is one way to look at it. On the other hand, some people probably do things without hesitation that would make me anxious. We all have our own things going on.

This article pertains to hardly anybody. Nobody I know because I don’t know anyone with this much in assets. Certainly wish these type of articles would work with realistic numbers and a normal couple. $2.647 million put away plus pensions ? Really? Get outta here! You’re addressing issues for the top 1/2 of 1%.

Your own blog would be a great place to write the types of articles that you like.

Seems good to me. I am 41 with 1.0 mil and a retirement (2 if I hang on for 7 more years in the Guard). We aren’t that rare…..

Hi Bob are you in Maryland or Virginia ? Thank you. SteveO

We are in Missouri and snowbirds in Florida. I’m trying to put something together as an update

I would love it if Bob could provide an update on the decisions he made after you analysed his financial situation all those years ago and let everyone know and how him and his wife have fared in the last 3 years. Stock market has been a good place to be for that last 3 years, just sayin’!

I agree it would be great to hear an update from Bob. It’s always interesting to hear how things turned out.

I commented in 2015 and can offer an update on myself.

My company changed the 401K rules in 2016 allowing unlimited withdrawals. So I worked to get myself laid off and succeeded. I got 9 months pay continuance.

I’ve been retired since then with my family in Thailand. I purchased health insurance policy for $2500/year for myself and the family is covered by universal government Health insurance.

I had put some cash aside,130K, to spend down then planned to withdraw from my 401K. But try as I might I’ve still got most of my cash and haven’t begun to withdraw from my 401K…..which I’m beginning to feel is a mistake.

I currently reinvest my $45k/year of dividends. I’ll claim a $1800/money pension at age 60 in 2.5 years. At age 62 illI claim my SS of $1800/mo so the kids can claim.

I have 1.7 M including the 401K.im trying to maximize my IRA to Roth conversions.

I can’t believe how easy the emotional adjustment has gone in regards to not having a job. It was certainly terrifying before I stopped working!

I learned a great deal from this original post and found I could identify with Bob, his fear and his situation. Once I realized that my personal withdrawal rate was probably 0% also I moved in a more determined direction.

Thanks Jeremy

Mike Hi, IMHO Keep the cash and spend down IRA or 401k. SteveO